How Much Catering Per Week Makes Sense? The Frequency Guide

1. Why Catering Frequency Is the Real Lever

In employee catering, much is discussed about the right model and the right budget, rarely about frequency. Yet the question of how often catering is offered per week is the most direct lever for both effect and cost.

The reason is simple: each additional catering day costs more in a plannable way, but does not automatically deliver the same added benefit. The first shared meal day of the week creates an anchor point, the second reinforces it. From the third or fourth day, the shared meal becomes routine, the additional effect on cohesion and appreciation flattens out, while costs keep running up linearly.

This article therefore deliberately differs from the model question. Which catering models exist for hybrid teams at all is set out in our article on office catering for hybrid teams. How the mix of catering and allowance shifts by office days is shown in the comparison of two versus five office days. Here it is solely about frequency: how many catering days per week really pay off.

2. Marginal Benefit: Why Days 1 and 2 Deliver Most

Catering per week follows a classic marginal-benefit pattern. The first days deliver the biggest effect per euro, after which each further day becomes relatively more expensive in relation to the added benefit.

One catering day per week turns an ordinary working day into an event. The team knows that Wednesday is for eating together, plans the day accordingly and uses it for exchange. The second day anchors this routine and makes the shared meal a fixed part of the week. It is exactly these two days that hold most of the effect on mood, retention and informal exchange.

From the third day, the ratio shifts. The shared meal is then everyday, which is good in itself, but the additional appreciation effect per further day declines. Costs, by contrast, rise equally with every day. That does not mean daily catering is wrong, but that it should be a conscious decision, driven by high presence rather than the feeling that more is automatically better.

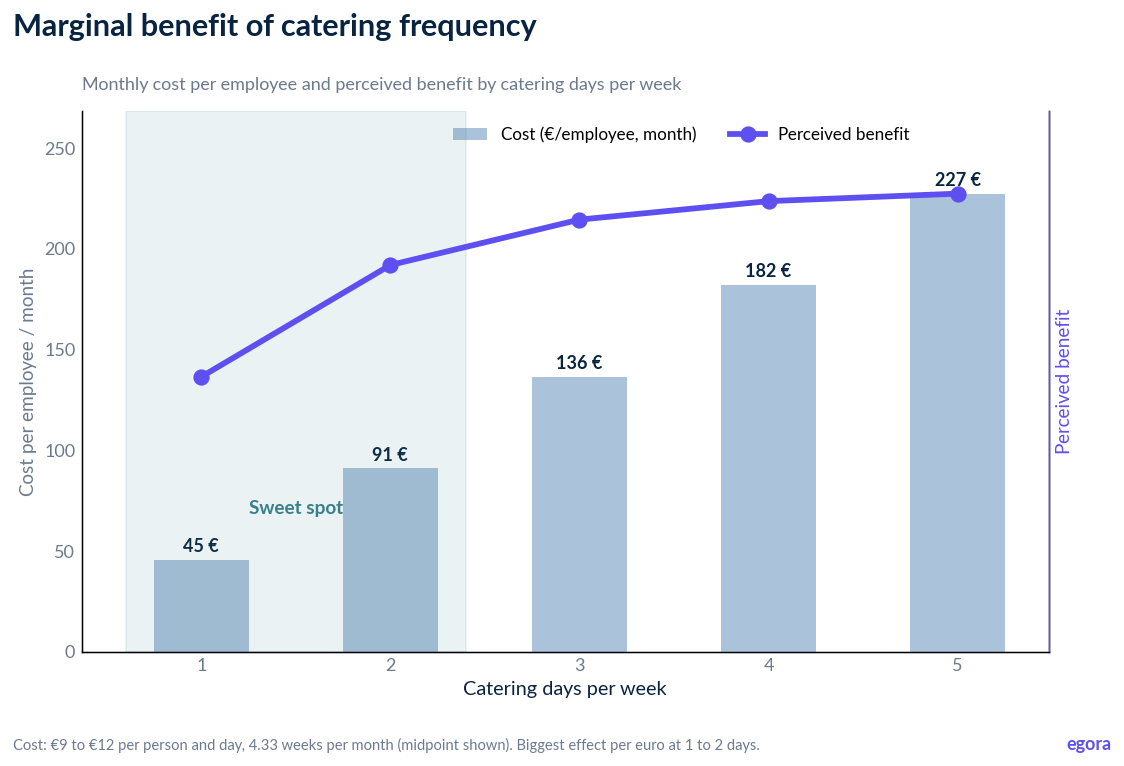

Figure 1: Marginal benefit of catering frequency. Costs rise linearly with each catering day per week, from around €36 to €52 per employee and month at one day to around €195 to €260 at five days (€9 to €12 per person and day, 4.33 weeks per month). Perceived benefit rises steeply at first and flattens from the third day. The biggest effect per euro lies at one to two days.

The figure makes the core message visible: the curves of benefit and cost diverge favourably at first and converge later. With a tight budget, the move is to start with one or two fixed days and increase only once presence and demand clearly justify it.

3. Frequency by Presence Profile

The sensible frequency depends directly on how often the team is in the office at all. Catering only works where people come together, so presence is the natural ceiling for catering days.

A team with two office days per week is best served with one to two catering days, ideally falling on the office days. More would miss reality, because on home-office days no one picks up the food. A team with three office days can sensibly use two to three catering days, depending on how busy the office days are. Only at full five-day presence does daily catering become the obvious option.

It matters to place catering days on the days with the highest attendance. If most people are in on Tuesdays and Thursdays, that is exactly where the catering belongs, not on a sparsely staffed Friday. That creates the largest common denominator and lets quantities be planned cleanly. How per-head costs relate to team size and frequency is explored in our article on the budget per employee.

Plan Catering Frequency for Your Team

- Recommended catering days per presence profile

- Catering placed on the best weekdays

- Realistic cost per employee and month

- Flexible providers for your locations

4. What Catering Per Week Costs

For HR and finance, the figure that counts is cost per head and month. It follows directly from the frequency, the price per person and the number of weeks in the month.

The basis for calculation is around €9 to €12 per person and catering day, plus 4.33 weeks per month. One catering day per week therefore costs about €36 to €52 per employee and month. Two days come to around €78 to €104, three days to around €117 to €156, and five days of full presence to around €195 to €260 per employee and month. The range depends mainly on whether a simple lunch concept from €9 or a higher-value offer at around €12 is chosen.

These figures show why frequency is the dominant cost driver. The jump from one to two days doubles the budget, the jump from two to five days more than doubles it again. Choosing the frequency deliberately means steering the largest item in catering costs directly.

At the same time, the calculation is plannable and linear, which makes budgeting easier. A fixed frequency can be projected cleanly across the year and planned into staff overheads without nasty surprises.

5. Combining With the Meal Allowance on Non-Catering Days

Catering every working day is rarely necessary, because the days without catering do not have to stay empty. The meal allowance fills that gap, complementing the catering flexibly and independent of location.

On catering days the caterer provides a shared meal in the office, on the remaining days the allowance applies. This works especially well for hybrid teams, because the allowance is redeemed in the home office too and thus covers every working day. Claiming the full daily rate of €7.67 gets the maximum out of it, as our article on how to make the most of the meal allowance shows.

This combination is also the clean economic route. Instead of ordering expensive catering on sparsely staffed days that no one picks up, you pay specifically for the office days and give the flexible allowance for the rest. That way each day gets a fitting offer, without idle costs and without gaps. The strategic context is set out in our complete guide to employee catering.

6. Finding the Right Frequency: A Decision Aid

The right catering frequency can be determined in a few steps. What governs it: the number of office days, attendance on the strongest days, and the budget available per head.

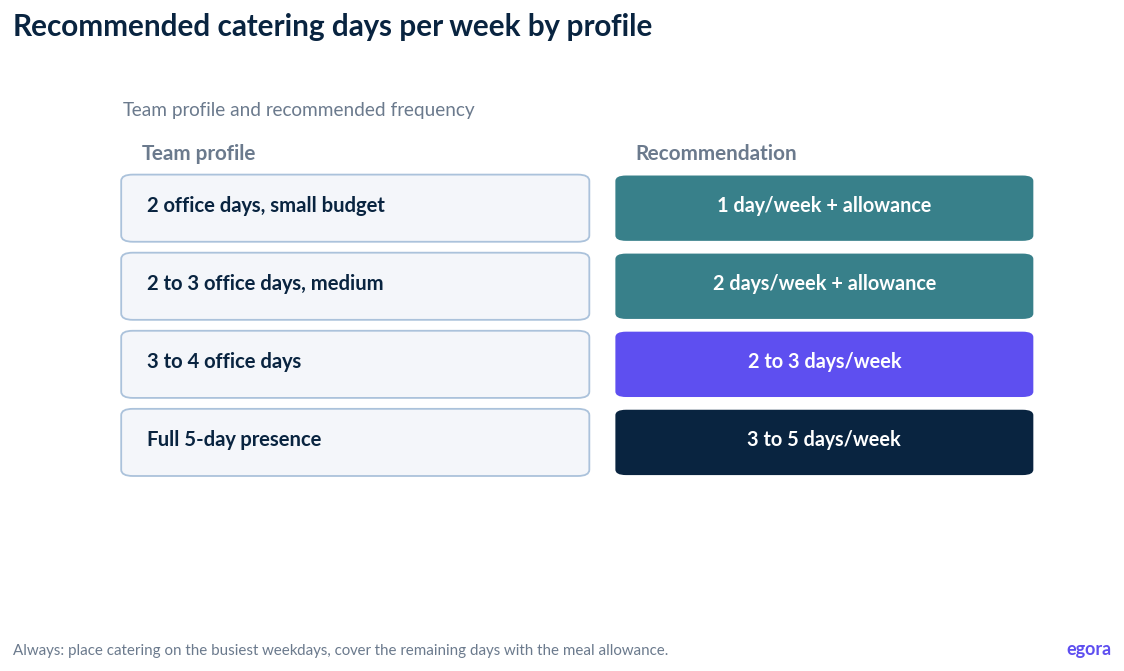

Figure 2: Decision matrix profile to frequency. Two office days, small budget: one catering day per week plus allowance. Two to three office days, medium budget: two catering days plus allowance. Three to four office days: two to three catering days. Full five-day presence: three to five catering days. In every case, place catering on the busiest weekdays and cover the remaining days with the meal allowance.

The matrix shows there is no universally right number, only a fitting ratio of presence, budget and occasion. One to two days is the economical starting point for most hybrid teams; higher frequencies pay off as presence rises.

If unsure, start deliberately low and increase after the first weeks once demand shows it. Too high a starting frequency is harder to walk back, because it quickly feels set in stone. A fixed, reliable rhythm counts for more than the sheer number of days.

Needs Analysis: Frequency and Budget

- Recommended catering days per week

- Cost per employee and month calculated

- Combination of catering and allowance

- Accounts for presence and locations

Conclusion

How much catering per week makes sense is answered not by the budget but by presence and marginal benefit. One or two fixed catering days deliver the biggest effect per euro and are the right starting point for most hybrid teams. Higher frequencies pay off as attendance rises, but should be chosen consciously, because costs rise linearly while the added benefit flattens out.

The economic sweet spot is the combination: catering on the strongest office days, meal allowance for the rest. For a hybrid team with two office days, that means two fixed catering days at roughly €78 to €104 per head and month, plus the €7.67 allowance on the remaining days. That mix lets you start without locking in, then adjust the frequency to real demand after the first few weeks.

FAQ

How often per week should you offer catering?

For most hybrid teams, one to two fixed catering days are the economical starting point, because that is where the biggest effect per euro arises. The frequency should fit the presence and can be increased as attendance rises.

Does daily catering pay off?

Only at high, ideally full presence. From the third day, benefit rises more slowly than cost, so daily catering should be a conscious decision rather than the default. At low presence you otherwise pay for food no one picks up.

What does catering cost per week and month?

At around €9 to €12 per person and day, one catering day per week costs about €36 to €52 per employee and month. Two days come to around €78 to €104, five days to around €195 to €260 per employee and month.

Fixed weekday or flexible?

A fixed weekday is almost always better. It creates a reliable routine, eases quantity planning and makes the shared meal an anchor point. Sporadic catering does not unfold this effect and is harder to calculate.

How do I combine catering with the meal allowance?

Catering on the busiest office days, meal allowance on the remaining days. The allowance applies independent of location, in the home office too, and thus covers every working day without idle costs for catering no one picks up.

Should you start high or low on frequency?

When in doubt, start low and increase after the first weeks once demand shows it. Too high a starting frequency quickly feels set in stone and is harder to walk back than a deliberately cautious one.

Similar articles

Get an individual menu suggestion today.